- Nvidia is giving its newest AI chips to small cloud providers that compete with major players like Amazon Web Services and Google.

- The company is also asking these small cloud providers for the names of their customers, allowing Nvidia to potentially favor certain AI startups.

- This move highlights Nvidia's dominance as a major supplier of graphics processing units (GPUs) for AI, which are currently in high demand.

- The scarcity of GPUs has led to increased competition among cloud providers and Nvidia's actions could further solidify its position in the market.

- This move by Nvidia raises questions about fairness and competition in the AI industry.

Nvidia investors expect the chip designer to report higher-than-estimated quarterly revenue, driven by the rise of generative artificial intelligence apps, while concerns remain about the company's ability to meet demand and potential competition from rival AMD.

Nvidia has established itself as a dominant force in the artificial intelligence industry by offering a comprehensive range of A.I. development solutions, from chips to software, and maintaining a large community of A.I. programmers who consistently utilize the company's technology.

Nvidia's impressive second quarter earnings have further solidified the bullish trend for AI-related cryptocurrencies, causing tokens such as FET, GRT, INJ, RNDR, and AGIX to surge by over 4% in the past 24 hours.

Artificial intelligence (AI) cryptocurrencies surged as Nvidia reported strong second-quarter earnings, exceeding estimates and reinforcing the bullish trend in AI technology.

Nvidia's sales continue to soar as demand for its highest-end AI chip, the H100, remains extremely high among tech companies, contributing to a 171% annual sales growth and a gross margin expansion to 71.2%, leading the company's stock to rise over 200% this year.

Nvidia's CEO, Jensen Huang, predicts that the artificial intelligence boom will continue into next year, and the company plans to ramp up production to meet the growing demand, leading to a surge in stock prices and a $25 billion share buyback.

Nvidia's sales have doubled, reaching a record high of $13.5 billion, driven by increasing demand for its AI chips, and the company expects sales to continue to rise, with plans to buy back $25 billion of its stock.

Nvidia, the AI chipmaker, achieved record second-quarter revenues of $13.51 billion, leading analysts to believe it will become the "most important company to civilization" in the next decade due to increasing reliance on its chips.

Nvidia's stock reaches a new high as Wall Street analysts praise the company's strong earnings, which demonstrate that the artificial-intelligence industry is continuing to drive its growth.

Nvidia's impressive earnings growth driven by high demand for its GPU chips in AI workloads raises the question of whether the company will face similar challenges as Zoom, but with the continuous growth in data center demand and the focus on accelerated computing and generative AI, Nvidia could potentially sustain its growth in the long term.

Nvidia's market capitalization surpassed that of the entire crypto market, reaching $1.18 trillion, after the chipmaker reported strong financial results, including double the net profit compared to the previous year, highlighting its leadership in AI hardware production and emphasizing the need for the crypto industry to embrace tokenization for similar growth.

Chip stocks, including Nvidia, experienced a selloff in the technology sector despite Nvidia's strong performance, leading to concerns that spending on AI hardware may be affecting traditional chip companies like Intel.

Nvidia's soaring stock price, driven by the booming demand for its data center graphics cards in the AI arms race, has led to a high valuation, making it an opportune time to consider investing in Advanced Micro Devices (AMD) as it could benefit from the growing demand for AI chips and potentially capture a significant share of the data center GPU market.

AMD investors may be feeling left out as the company struggles to match the financial growth and stockholder returns of its competitor, Nvidia, but there is still potential for AMD to narrow the gap in the generative AI market and offer solid returns in the long term.

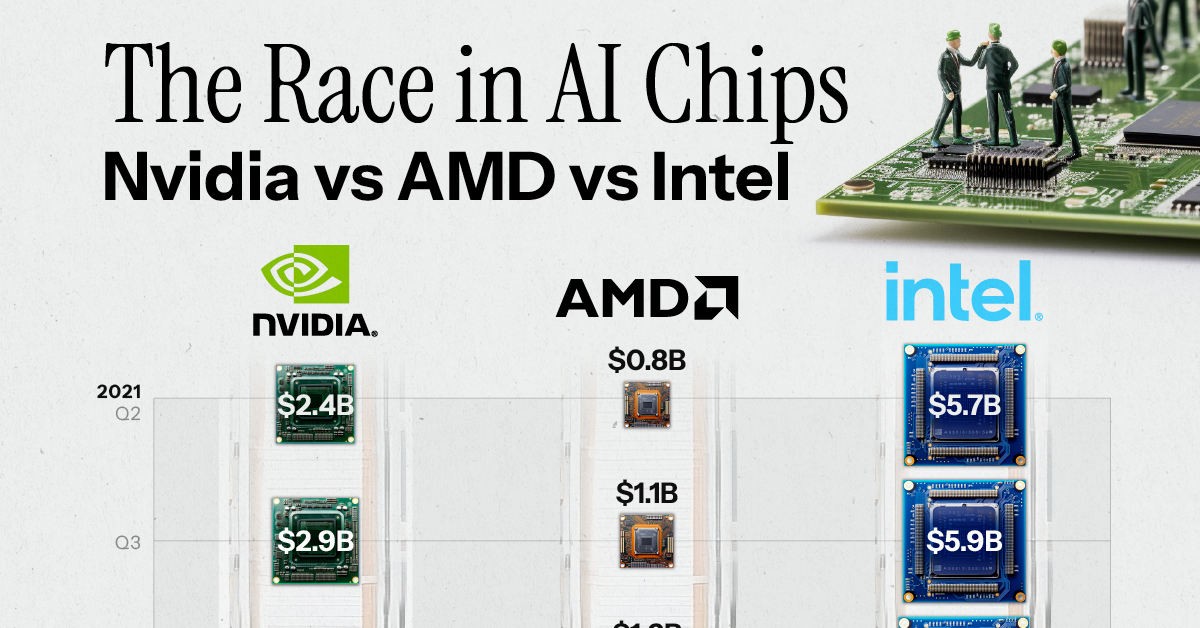

Nvidia's rivals AMD and Intel are strategizing on how to compete with the dominant player in AI, focusing on hardware production and investments in the AI sector.

Nvidia reported a strong quarter, with beats across three out of its four businesses, driven by strong demand for its data center segment and generative AI products, leading to record revenues and beating market consensus by 22%. However, there are concerns about the sustainability of this growth and the potential impact of competition in the future.

Artificial intelligence (AI) leaders Palantir Technologies and Nvidia are poised to deliver substantial rewards to their shareholders as businesses increasingly seek to integrate AI technologies into their operations, with Palantir's advanced machine-learning technology and customer growth, as well as Nvidia's dominance in the AI chip market, positioning both companies for success.

Nvidia's stock is reaching all-time highs, but one analyst argues it is still cheap, as it trades at a modest premium compared to other AI-related stocks and has a lower multiple than industry stalwarts like Amazon, Adobe, and Microsoft.

Advanced Micro Devices (AMD) stock is rising as investors recognize its potential in the artificial intelligence (AI) hardware market, making it a strong competitor to Nvidia, especially with the launch of its M1300X AI chip in the third quarter of 2023.

Nvidia predicts a $600 billion AI market opportunity driven by accelerated computing, with $300 billion in chips and systems, $150 billion in generative AI software, and $150 billion in omniverse enterprise software.

Semiconductor stocks, particularly Nvidia, have outperformed the market due to the high demand for chips in AI applications, making Nvidia the better AI stock to buy compared to Intel.

Nvidia's rapid growth in the AI sector has been a major driver of its success, but the company's automotive business has the potential to be a significant catalyst for long-term growth, with a $300 billion revenue opportunity and increasing demand for its automotive chips and software.

Nvidia's success in the AI industry can be attributed to their graphical processing units (GPUs), which have become crucial tools for AI development, as they possess the ability to perform parallel processing and complex mathematical operations at a rapid pace. However, the long-term market for AI remains uncertain, and Nvidia's dominance may not be guaranteed indefinitely.

Nvidia and Amazon, both of which recently underwent stock splits, are positioned for long-term growth in the AI industry due to their focus on infrastructure and strong economic moats, with Amazon being the safer pick due to its diversified business model and cost-cutting efforts.

Despite a significant decline in PC graphics card shipments due to the pandemic, Advanced Micro Devices (AMD) sees a glimmer of hope as shipments increase by 3% from the previous quarter, indicating a potential bottoming out of demand, while its data center GPU business is expected to thrive in the second half of the year due to increased interest and sales in AI workloads.

Nvidia's dominance in the computer chip market for artificial intelligence has led to a significant decline in venture funding for potential rivals, with the number of U.S. deals dropping by 80% from last year. The high cost of developing competing chips coupled with Nvidia's strong position has made investors wary, resulting in a pullback in investment.

Nvidia's stock has seen a 200% gain this year, highlighting the lucrative potential of the artificial intelligence trade.

Nvidia, the leader in AI infrastructure, has experienced substantial growth and is expected to continue growing, but investors should be cautious of the stock's high valuation and potential volatility.

Nvidia, with its dominant market share and potential for growth in the AI industry, is considered a worthwhile investment despite its high valuation. On the other hand, C3.ai has failed to capitalize on the AI boom and presents a poor investment opportunity.