Summary: U.S. markets end mixed with Nasdaq up over 1% due to the surge in technology stocks, Asian markets show positive gains with Japan's Nikkei 225 rising 1.05%, and European markets are higher as the tech sector gains ahead of the U.S. Federal Reserve's Jackson Hole gathering, while crude oil prices decrease slightly.

Stock indices finished the trading session in the green, with gains seen in the Nasdaq 100, S&P 500, and Dow Jones Industrial Average. However, Texas manufacturing experienced a downturn in August, and gas prices have slipped across the country. U.S. stock futures are trending higher, and traders are awaiting key economic releases and earnings reports this week. In Asian markets, indices ended higher, but Evergrande Group's shares plunged while Xpeng's shares rallied.

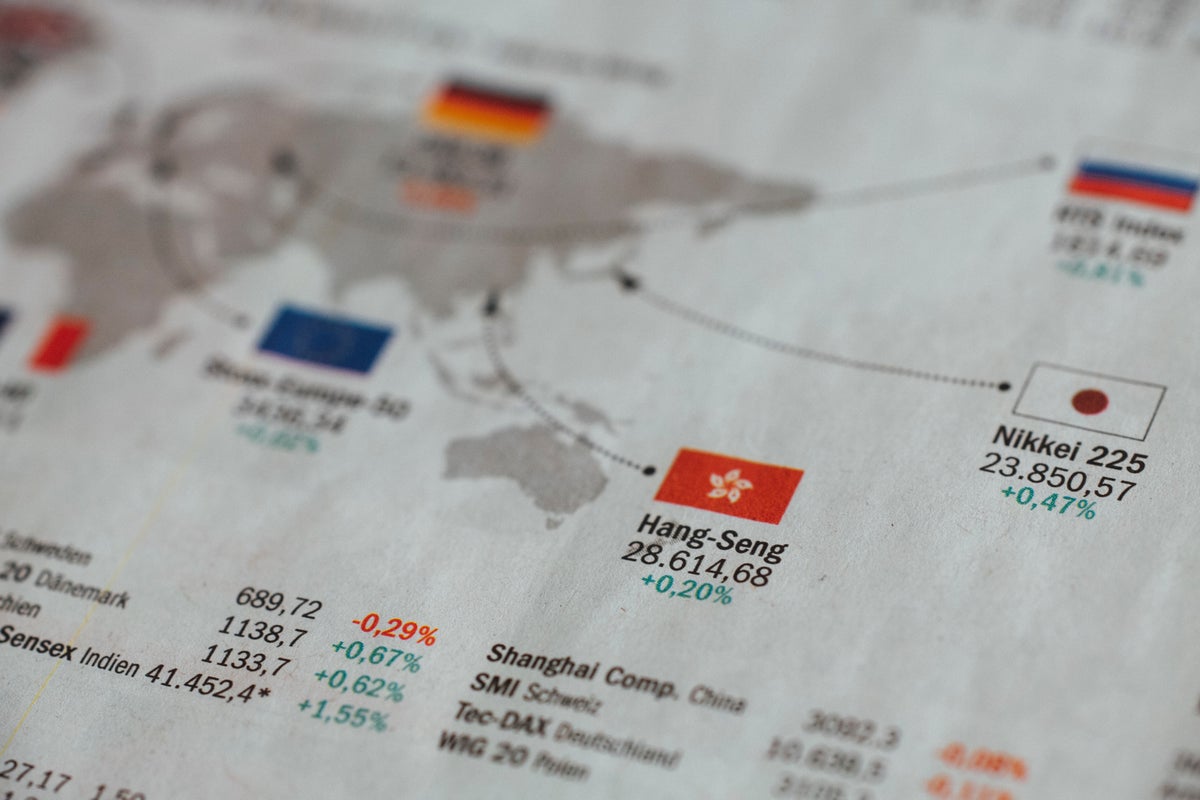

Summary: The US markets ended mixed after the release of the latest jobs report data, with the economy adding 187,000 jobs in August but seeing an increase in unemployment, while in Asia, Japan's Nikkei 225 closed higher, Australia's S&P/ASX 200 was down, and China's Shanghai Composite and Shenzhen CSI 300 declined. Additionally, European markets saw declines, and commodities such as crude oil, natural gas, gold, silver, and copper experienced varying price movements.

Wall Street's main indexes fell in choppy trade due to rising Treasury yields and weak services activity in China, while gains in energy stocks limited losses; however, expectations of a pause in Fed monetary tightening boosted growth stocks.

U.S. stocks slipped as worrying data out of China and a spike in oil prices following the extension of Saudi Arabian production cuts weighed on the market. The Dow Jones Industrial Average fell 0.6%, while the S&P 500 lost 0.4% and the Nasdaq dipped 0.1%.

European stock markets weakened on Thursday due to signs of slowing growth in Europe and China, as well as concerns about future Federal Reserve tightening. German industrial production fell more than expected, adding to the struggles of the eurozone's largest economy. China's exports and imports also fell in August, indicating continued pressure on its manufacturing sector. Additionally, stronger-than-expected US inflation data raised concerns about sticky inflation. Oil prices fell as signs of slowing Chinese growth overshadowed a draw in US inventories.

U.S stocks are recovering from losses, with the S&P 500 and Dow Jones Industrial Average both up 0.4%, as tech stocks lead the market higher and investors await key data on inflation this week.

Global markets ended higher as energy stocks climbed supported by Saudi Arabia and Russia's decision to extend supply cuts, while Wall Street's key indexes saw weekly declines due to investor concerns over interest rates and anticipation of upcoming U.S. inflation data. In Asian markets, Japan's Nikkei 225 ended down, Australia's S&P/ASX 200 was up, and Chinese shares rose following improved data on consumer price inflation. The Eurozone's economic growth outlook has been downgraded by the European Commission, and crude oil prices fell.

Stock indices closed in the red, with the Nasdaq 100, S&P 500, and Dow Jones Industrial Average all experiencing declines, while the technology sector underperformed and the energy sector led the session. The U.S. 10-Year Treasury yield dropped, while the Two-Year Treasury yield increased. The Small Business Optimism Index for August decreased, with inflation cited as a major concern among small business owners. Stocks opened lower on Tuesday, and U.S. futures trended lower as well. This week's focus will be on the Consumer Price Index and Producer Price Index data, which could impact the Federal Reserve's decision on rate hikes. Oracle's stock fell after missing sales estimates, while Casey's General and Tesla saw gains. JPMorgan's CEO criticized new Basel III regulations, and European indices traded in the green. In Asia-Pacific, markets ended mixed as traders await U.S. inflation data.

Dow Jones futures, along with S&P 500 futures and Nasdaq futures, were unchanged after hours as the stock market rally experienced losses, with the S&P 500 and Nasdaq dropping below the 50-day line, while energy stocks led and software retreated. Apple stock fell after unveiling the iPhone 15 and other products, while stocks such as Salesforce, Alphabet, General Electric, Shopify, and Nvidia remained in or near buy areas. The CPI inflation report and Adobe earnings are potential market catalysts.

Asian stock markets fell as Wall Street experienced a decline, with investors preparing for key US inflation data, and a spike in oil prices added to concerns about persistent price pressures and the interest rate outlook.

US stocks slumped as reports of China's recovering economy caused concern, potentially impacting global stock exchanges, while the US auto workers' strike and oil price rallies also contributed to market fluctuations.

Asia-Pacific markets fell as traders awaited the Reserve Bank of Australia's policy meeting minutes, while European markets were weighed down by a spike in corporate lending rates; meanwhile, Goldman Sachs predicts that the Fed is done hiking this year and the recent increase in oil prices could benefit London's prime office real estate market.

U.S. stock markets closed lower amid risk-off sentiment as the Federal Reserve began its two-day monetary policy meeting, while Asian markets, including Japan's Nikkei 225 and Australia's S&P/ASX 200, experienced declines; however, European markets, including Germany's DAX and the U.K.'s FTSE 100, traded higher.

The U.S. stock markets closed in the red as the Federal Reserve kept the federal funds rate unchanged, leading to losses in sectors such as communication services and information technology, while Asian stocks fell due to concerns over higher U.S. interest rates.

Shares in Asia and European equity futures fell while Treasury yields and the dollar rose, indicating that investors have yet to fully adjust their expectations for interest rates.

Asia-Pacific markets fell ahead of China's industrial data and Australia's inflation figures, while the US experienced a sell-off after disappointing economic data, causing the Dow Jones Industrial Average to fall below its 200-day moving average for the first time since May. Additionally, oil prices continue to rise, putting crude on track for its best quarter in over a year, and Tesla shares dropped after reports of an EU investigation into whether the company and other European carmakers are receiving unfair subsidies for exporting from China.

The U.S. stock market has experienced a decline due to conflicting economic news and a surge in bond yields, which may be driven by factors other than data, such as fiscal deficits and central bank policies.

Wall Street turned lower as concerns over interest rates, rising oil prices, and a possible government shutdown weighed on the market, with the Dow Jones and S&P 500 both experiencing losses.

Asia-Pacific markets mostly fell due to an increase in Treasury yields and oil prices, leading to a decline in investor sentiment on Wall Street, with Hong Kong's Hang Seng index sliding 1.41% after shares of Evergrande were suspended.

U.S. stocks mostly fell as investors considered the latest inflation data from the Federal Reserve, marking the end of a turbulent month for the market.

Stocks mostly fell in the U.S. on Friday, with the S&P 500 and Dow Jones Industrial Average declining, while the Nasdaq Composite inched up; all three indexes ended the month of September in the red, with the S&P and Nasdaq experiencing their worst monthly performance since December, and the Dow having its worst showing since February.

Summary: The U.S. stock market had a bad quarter, with all indexes falling, while the World Bank lowered its growth forecast for developing economies in East Asia and the Pacific, and China's demand for commodities continues to grow despite the downgrade. Additionally, a last-minute spending bill was passed to avoid a government shutdown, and this week's focus will be on the labor market.

Stock markets ended mixed as investors processed the effects of the U.S. inflation report on the Federal Reserve's interest rate policy, with the S&P 500 declining by 0.27% and the Nasdaq Composite gaining 0.14%; in Asian markets, Japan's Nikkei 225 settled lower by 0.31% while Australia's S&P/ASX 200 slid 0.22%; in Europe, the STOXX 600 index was down 0.42% with Germany's DAX declining 0.25%, France's CAC 40 sliding 0.36%, and the U.K.'s FTSE 100 trading lower by 0.45%; and in commodities, Crude Oil WTI and Brent gained 0.82% and 0.89% respectively, while Gold traded lower by 0.88%.

The stock market declined as the Dow lost 430 points and the Nasdaq lost 248 points, with the overall market being negatively affected by a higher 10-year bond yield and robust labor force data, while political turmoil in the House of Representatives and the possibility of a government shutdown added to the market's uncertainty.

The U.S. stock market ended mixed, with the S&P 500 remaining unchanged, while the Nasdaq saw gains due to Nvidia's shares jumping following Goldman Sachs' endorsement, and global markets experienced losses, including Japan's Nikkei 225, Australia's S&P/ASX 200, and Hong Kong's Hang Seng index.

Stock indices finished in positive territory, with the Nasdaq 100, S&P 500, and Dow Jones Industrial Average all posting gains, while the energy sector experienced losses; meanwhile, the U.S. 10-Year Treasury yield decreased and the Two-Year Treasury yield also saw a decline. The Factory Orders report showed an increase in new purchase orders placed with manufacturers, beating expectations. The ISM Non-Manufacturing Purchasing Managers' Index indicated a slight contraction in the non-manufacturing sector, and the ADP jobs growth data showed a slowdown in job growth and wages. U.S. Futures opened lower following higher-than-anticipated JOLTs jobs opening data. Asian markets ended mixed, while European indices traded in the red.

The dollar weakened and global equities dipped as investors grappled with U.S. unemployment data suggesting a tight labor market and the Federal Reserve's commitment to higher interest rates, while European stocks rebounded from losses.

Stocks on Wall Street opened lower after the US jobs report exceeded expectations, raising concerns that the Federal Reserve may raise interest rates; the Dow Jones was down 0.3%, the S&P 500 lost 0.4%, and the Nasdaq Composite dropped 0.5%.

U.S. stock markets closed higher on Friday due to strong job creation, leading to discussions about a potential Federal Reserve interest rate hike; Asian markets, including Japan, Australia, and China experienced mixed results; European markets were mostly positive; commodities such as crude oil and gold saw an increase in prices; and U.S. futures and forex showed a decline and mixed results respectively.

Dow Jones futures rose slightly while S&P 500 futures and Nasdaq futures fell; Treasury yields retreated and crude oil spiked as U.S. sanctions on Russian crude sales tightened; UnitedHealth, JPMorgan Chase, Wells Fargo, Citigroup, PNC Financial Services, and BlackRock reported their earnings; the stock market rally retreated after an inflation report and a poorly received Treasury auction; Apple and Microsoft stocks edged higher while Google and Meta Platforms fell; Dow Jones futures rose slightly; the 10-year Treasury bond yield fell; the stock market rally struggled at key levels; growth ETFs slumped; megacap stocks like Apple, Microsoft, Google, Meta, Nvidia, Amazon, and Tesla were down a fraction; investors should be cautious and ready to reduce or exit positions if necessary.

US stocks fall as fears of war in the Middle East and hopes for stronger profits at big US companies collide in financial markets; oil prices rise and Treasury yields fall, creating uncertainty in the market.

The U.S. stock markets closed in the red due to rising bond yields and higher-than-expected inflation, while Asian markets also experienced declines amid concerns of prolonged higher interest rates.

U.S. stock markets closed mixed as declining consumer confidence and Middle East tensions overshadowed positive earnings from major banks, while Asian markets saw losses ahead of crucial inflation data, and European markets were mostly down.

Stocks rise and bond prices decline as markets focus on corporate earnings and the strength of the U.S. economy, rather than Middle East tensions, signaling a reversal of last week's risk-off sentiment.

Stock markets in the US closed higher, driven by optimism over earnings season, while Treasury yields rose due to concerns over the conflict between Israel and Hamas; Asian markets followed suit, with Japan's Nikkei 225 closing higher and Australia's S&P/ASX 200 recording gains, while European markets saw mixed results; in commodities, crude oil prices were relatively stable, while gold and silver prices increased slightly; and US futures indicated a slight decline.

Stock markets in the US closed mixed on Tuesday, with positive economic data and strong Q3 earnings suggesting a continued tight monetary policy by the Federal Reserve, while Asian markets saw a mix of gains and declines, with Japan's Nikkei 225 and Australia's S&P/ASX 200 closing higher, and China's Shanghai Composite and Shenzhen CSI 300 declining; European markets also saw declines, and commodities such as crude oil, gold, and silver saw gains.

The U.S. stock markets decreased due to rising Treasury yields and investor evaluations of corporate earnings, while Asian markets, including Japan's Nikkei 225 and Australia's S&P/ASX 200, also experienced declines; the European STOXX 600 index and Germany's DAX also decreased, while crude oil, gold, and silver prices fell.

Asian markets fell and oil prices rose as concerns about a potential ground invasion in Gaza by Israel increases the risk of a wider conflict in the Middle East, compounded by the Federal Reserve indicating a pause in interest rates but leaving the possibility of future hikes.

Asian stock markets fell on Friday, following the lead of U.S. markets, as bond yields increased and Federal Reserve Chairman Jerome Powell's remarks weighed on equities; South Korea's KOSPI Composite Index and Hong Kong’s Hang Seng Index were among the top losers, while Japanese inflation data showed price rises easing but still above the Bank of Japan's target rate of 2%.

U.S. stock markets closed in the red due to concerns over interest rate increases and the Israel-Hamas conflict, while Asian markets also experienced declines, with Japan's Nikkei 225, Australia's S&P/ASX 200, and China's Shanghai Composite all closing lower.